Dear PGM Blog reader,

In this weekend blog article, we want to take the opportunity to discuss with you why Investing in Norway’s StatOil can be lucrative for income investors.

INTRODUCTION:

Statoil ASA, (STL.OL), a Norwegian multinational oil and gas company headquartered in Stavanger, Norway, is a fully integrated petroleum company with operations in thirty-six countries.

Statoil was formed by the 2007 merger of Statoil with the oil and gas division of Norsk Hydro.

![]()

By revenue, Statoil is ranked by Oil & Gas 360 (2016) as the world’s eleventh largest oil and gas company and according with Forbes it is the twenty-sixth largest company, regardless of industry, by profit in the world.

As of 2013, the Government of Norway is the largest shareholder in Statoil with 67% of the shares, while the rest is public stock.

STATOIL Q1-2017 EARNINGS REPORT:

On Thursday May 4th, the company reported underlying operating profits of US$ 3.3billion in the first quarter of this year compared with US$ 857 million a year earlier, which is an increase of more than 380 percent.

The Norwegian group was also helped by the rise in oil prices from the 12-year lows recorded at the start of 2016 and increased output, including the highest production from its home market in five years.

Total revenue surged 53.3% year over year to US$15.5 billion.

Q1-2017 Operational Performance:

- Total equity production of liquids and gas was 2,146 thousand barrels of oil equivalent per day (MBOE/d), up 4.5% from 2,054 MBOE/d in the year-ago quarter.

- New production from the start-up and ramp-up of various fields, effects of redetermination and stronger operational performance were offset by divestments as well as expected natural decline and cease of production from various fields

- The underlying production growth in the quarter, after adjusting for divestments, was 5% year over year.

- The company made seven discoveries from nine exploration wells drilled. Adjusted exploration expenses in the quarter were US$202 million compared with US$280 million in the first quarter of 2016.

Financials:

- The Company’s cash flow from operations amounted to US$5,970 million in Q1-2017 compared with US$2,205 million in Q4-2016.

- Net debt to capital employed at the end of the quarter was 30%.

- Organic capital expenditure was US$2.2 billion in the first three months of 2017.

StatOil’s CEO Statements:

During the presentation of the company’s financial results , the CEO, Mr. Eldar Saetre said:

Our solid financial result and strong cash flow across all segments was driven by higher prices, good operational performance and an organic production growth of 5 per cent.

Our production from the Norwegian Continental Shelf was at its highest level in five years, driven by high regularity and ramp-up of new fields.

Our international portfolio delivered positive results and cash flow per barrel after tax on par with our Norwegian portfolio.

We continue to capture efficiency gains and are on track to deliver an additional billion dollars in annual improvements in 2017.

PGM CAPITAL ANALYSIS & COMMENTS:

Outlook:

Statoil expects organic capital expenditure of US$11 billion in 2017. Organic production growth for the period 2016-2020 is expected at a CAGR of about 3%.

The company expects equity production for 2017 to be about 4-5% above the 2016 levels. Total exploration activity level is expected to be around $1.5 billion in 2017.

Eldar Saetre, Statoil’s chief executive, told investors two months ago he was the most optimistic he had ever been about investment opportunities in his 36 years at the company.

Dividend:

From 12 May 2017, the shares in Statoil at Oslo Stock Exchange (Oslo Børs) will be traded ex dividend USD 0.2201 and ex rights to participate in the dividend issue for fourth quarter 2016.

Record date at New York Stock Exchange and Oslo Børs is 15 May 2017.

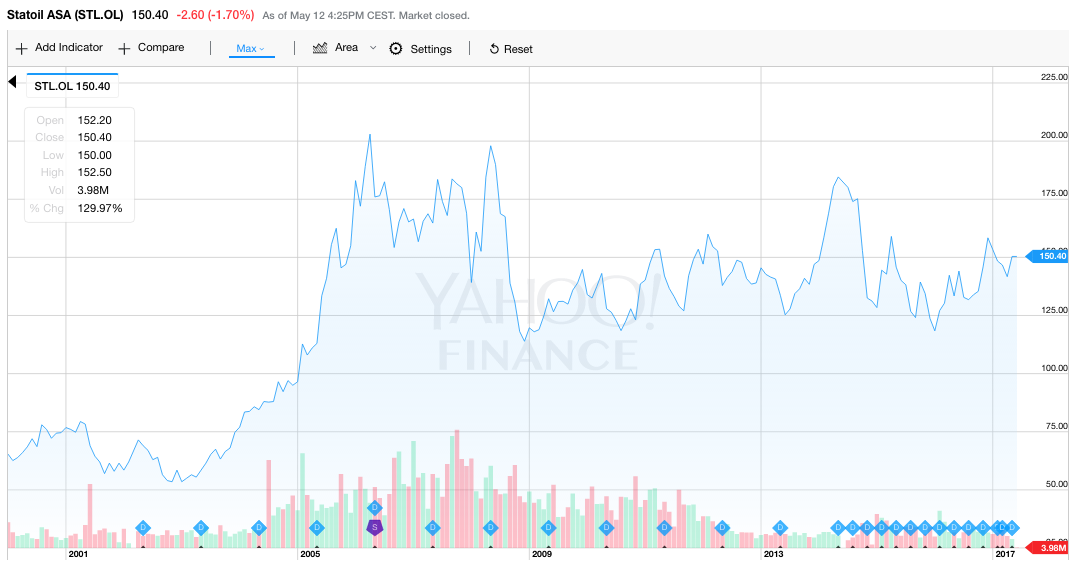

Based on the closing price of NOK 150.40 per share on Friday May 12, the shares of the company have a dividend yield is 5.03%.

As can be seen from below chart the shares of the company, in NOK, over the last 12 years have showed a very low volatility.

Below chart shows us that the exchange rate of the NOK against the USD is currently at a 10-year low against the USD.

Norway is a high developed country with a AAA credit rating, which in the last 10 years is in the top five of the; HDI, Good Governance and GDP per Capita ranking.

Based on the above, and fundamentals of the company and its very healthy dividend yield of 5.03%, we have a BUY rating on the stock of the Company and consider it a good investment for income investors, in the current area of low to negative interest rates.

Last but not least, before taking any investment decission, always take your investment horizon and risk tolerance into consideration and keep in mind that commodity prices as well as the securities of their producers, can be very volatile and that sharp corrections might happen in the short term.

Yours sincerely,

Eric Panneflek