Dear PGM Capital blog readers,

In this weekend blog edition, we want to discuss some of the most important events that happened in the global capital markets, the world economy and the world of money in the week of June 12, 2017:

- The FED raised key interest rates in the USA on, Wednesday June 14, 2017.

- Global Markets down after FED rate hike.

- Crude Oil slumps to 7-month low.

FED RAISE KEY RATES ON JUNE 14, 2017:

On Wednesday, June 14, at the end of its FOMC, meeting, as expected the USA Federal Reserve raised its benchmark interest rate to a range between 1 percent and 1.25 percent.

It is the third consecutive quarterly increase as the Fed continues to retreat from its economic stimulus campaign. The FED has now raised rates by a full percentage point since the financial crisis in 2008.

In new language, the FED’s statement also stressed that its inflation target is symmetric, in an acknowledgment that price growth could surpass its 2 percent target without forcing the central bank to clamp down precipitately.

GLOBAL MARKETS DOWN AFTER FED RATE HIKE:

NASDAQ:

A slide in technology stocks pulled down the Nasdaq Composite on Wednesday and the S&P 500 ended slightly lower, as investors worried about the pace of economic growth after weaker-than-expected inflation numbers and an interest rate hike from the Federal Reserve.

As can be seen from below chart, the Nasdaq cut its loss in more than half in a late rebound, having earlier fallen 1 percent.

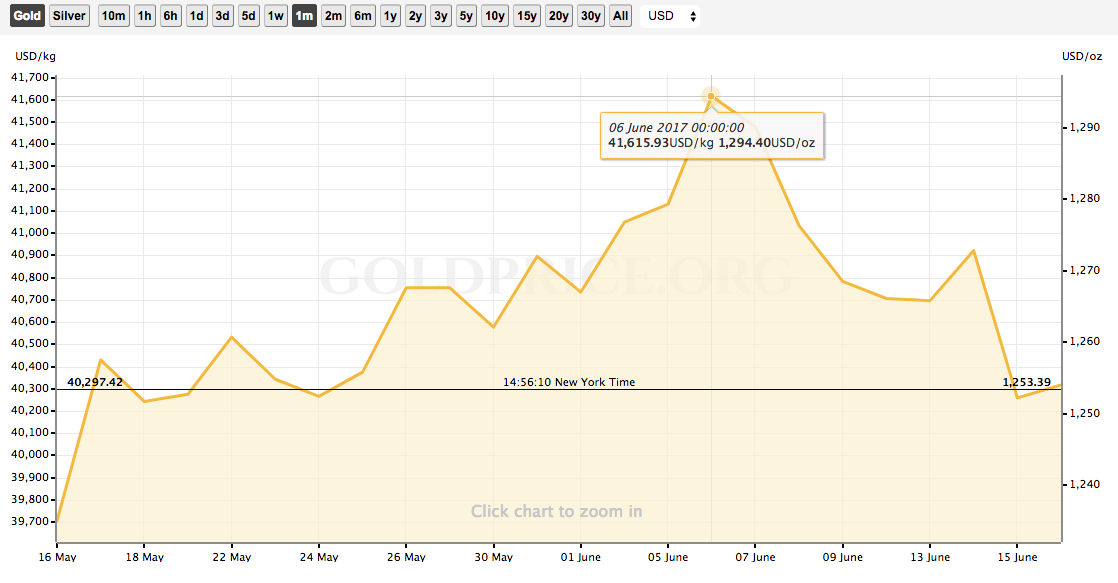

GOLD:

As can be seen from below chart, in anticipation of a FED rate hike, Gold prices fell from almost US$ 1,300.00 an ounce of Tuesday June 6, to close the trading week at US$ 1,253.39 an ounce.

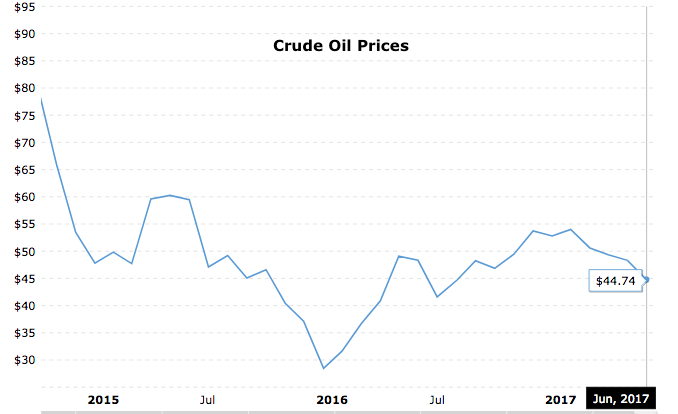

CRUDE OIL PRICES AT SEVEN MONTH LOW:

On Wednesday June 14, 2017, the EIA (U.S. Energy Information Administration) released its weekly petroleum status report. It reported that US crude oil inventories fell by 1.7 MMbbls (million barrels) to 511.5 MMbbls on June 2–9, 2017

Based on this Oil prices tanked, West Texas Intermediate crude Oil futures fell 3.7%, on Wednesday, June 14, to settle at US$ 44.73 a barrel, as can be seen from below chart.

PGM CAPITAL ANALYSIS & COMMENTS:

By raising the interest rates, the FED is also increasing the interest payment of the highly indebted USA.

Over the next decade, interest payments on the US government debt are projected to be the fastest growing part of the federal budget.

Recent market activity and Federal Reserve actions already suggest interest rates will rise; yields on the 3-month Treasury bill doubled in the past 5 months, while yields on the 10-year Treasury note rose 50 percent.

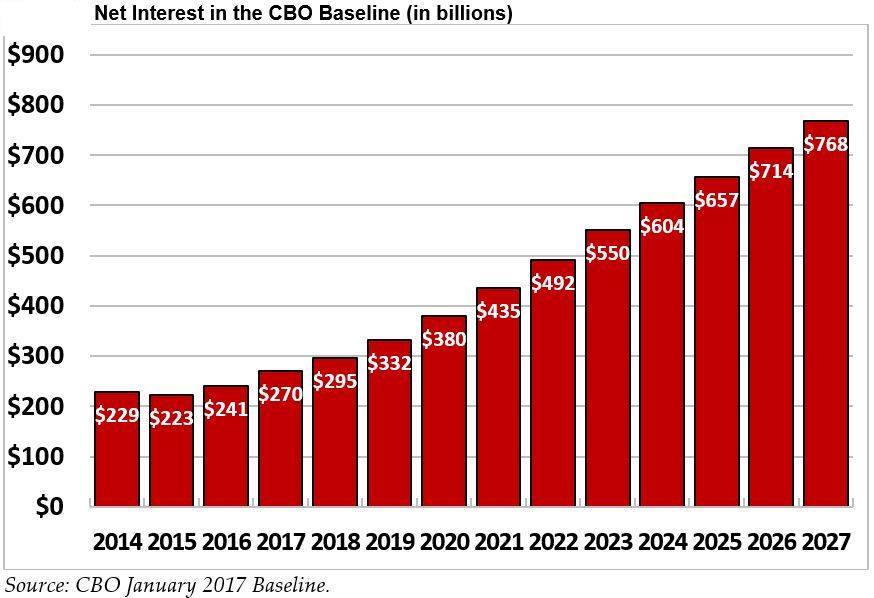

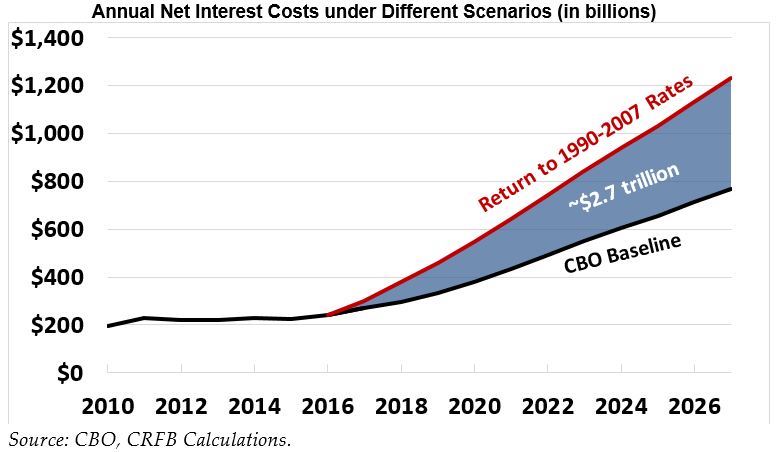

In combination with rising debt levels, this increase in rates will lead interest payments to grow rapidly. Under current law, the Congressional Budget Office (CBO) projects interest payments to nearly triple in nominal dollars and double as a percent of GDP – from US$270 billion and 1.4 percent of GDP in Fiscal Year (FY) 2017 to US$768 billion and 2.7 percent of GDP by FY 2027, as can be seen from below chart.

Even with today’s low interest rates, deficits have risen off their post-recession lows, are already large, and are projected to rise further over the next decade. As debt continues to grow and interest rates return to more normal levels, interest spending is slated to be the fastest growing part of the budget and will ultimately crowd out other important priorities. Adding to the debt, even for worthwhile policy changes, would only accelerate the growth in interest costs.

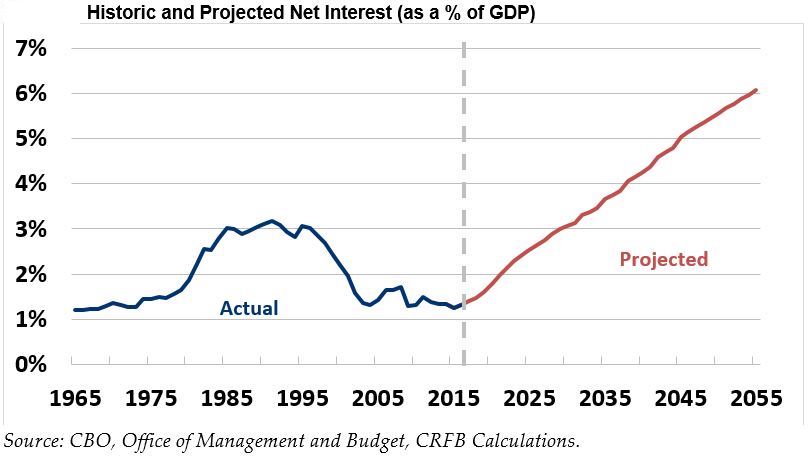

Over the long term, interest costs of the USA will grow from 1.4 percent of GDP today to 3.8 percent in two decades and 6.3 percent in four decades as can be seen from below chart.

On top of this CBO estimates that if interest rates were 1 percentage point higher annually than projected through 2027 – a level that would still be less than the pre-recession average – debt would be US$1.7 trillion higher, or 6 percent of GDP, higher.

This suggests that if interest rates were to return to roughly their pre-recession averages, debt would be about US$2.8 trillion higher, or 10 percent of GDP as can be seen from below chart.

Based on the above, we believe, that the current FED interest increase cycle, might trigger the next recession and due to this will be short-lived. If the USA entered a recession with such a debt burden, the only way out will be, diluting of this debt, by creating inflation via massive money printing. Due to this we stick to our advise to avoid the US-Dollar and to accumulate Gold and other precious metals on any dip.

Last but not least, before taking any investment decision, always take your investment horizon and risk tolerance into consideration and keep in mind that the market can remain irrational longer than you can remain solvent and that sharp corrections might happen in the short term.

Yours sincerely,

Eric Panneflek